Following twenty-three years of radical federalism under Colombia’s 1863 Liberal Constitution, a coalition of moderate liberals and conservatives triumphed in the 1884 general elections. The victorious presidential candidate, Rafael Nuñez—a former liberal who had become a leading figure in this coalition—sought to dismantle key Liberal reforms, particularly fiscal federalism. Regional governments dominated by radical liberals mounted armed resistance against these centralizing policies, which threatened their political and fiscal autonomy. The federal government ultimately crushed these rebellions, assumed direct control over state administrations, and in 1886 replaced the existing constitution with a new charter that dramatically reshaped Colombia’s governance structure. This constitutional overhaul transformed regional entities (henceforth termed departamentos) by stripping them of tax and budgetary autonomy, consolidating fiscal authority in Bogotá—the dual capital of both the nation and the Department of Cundinamarca.

This article examines how this centralization process influenced the development of local public finance systems in Cundinamarca, one of Colombia’s most economically dynamic regions. Through quantitative analysis of reconstructed fiscal series—drawn from treasury reports, legislative budgets, and contemporary newspapers—we trace long-term patterns in taxation and social expenditure, with particular attention to public beneficence programs where Cundinamarca emerged as an institutional pioneer during the federal era.

Colombian fiscal historiography demonstrates that mid-nineteenth century local governments actively worked to eliminate colonial-era taxes while expanding provision of public goods—even amid chronic political instability and civil conflict. Cundinamarca’s 1870s innovation of dedicated charity taxes exemplifies this trend, as regional administrations increasingly encroached on domains traditionally monopolized by the Catholic Church, particularly education and healthcare. Our study evaluates how the 1886 Constitution’s centralizing reforms impacted these local fiscal arrangements, revealing that Cundinamarca retained surprising administrative flexibility—continuing to shape its tax policies and even expand social spending until at least 1910 despite the new unitary system.

Decentralization theory posits that local governments allocate public resources more efficiently than central authorities, benefiting from superior local knowledge and stronger accountability mechanisms (Oates 1999; Tiebout 1956). However, institutional economists (Acemoglu et al. 2001, 2005) counter that developmental outcomes depend less on administrative scale than on whether institutions incentivize broad participation: inclusive systems foster growth by encouraging investment and innovation, while extractive institutions concentrate power and stifle economic potential.

Cundinamarca’s late nineteenth-century experience substantiates this institutionalist perspective. The department’s sustained fiscal autonomy and expanded social expenditures—even after national centralization—demonstrate how subnational governance structures can cultivate developmental state capacity. Its pioneering charity taxes reflect precisely the sort of inclusive institution-building that Acemoglu’s framework identifies as growth-conducive.

This case also illuminates broader Latin American state formation patterns. Colombia’s 1886 centralization occurred amidst regional struggles to balance fiscal consolidation with effective public goods provision—a tension exacerbated by persistent political violence. Recent scholarship nonetheless questions decentralization’s presumed advantages: central governments may achieve superior economies of scale (Stein 1998), while localized systems risk inefficiency from limited technical capacity (Iimi 2005) or corruption (Bardhan & Mookherjee 2005; Fisman & Gatti 2002).

Effective subnational governance requires balancing two state functions: revenue extraction and public goods provision (Dincecco & Katz 2012). Tax systems depend on both voluntary compliance (rooted in perceived legitimacy) and coercive enforcement—a dialectic of rational consent and imposed discipline. Where taxpayers recognize tangible benefits from expenditures—as in decentralized systems with visible local investments—compliance improves markedly. Colombia’s nineteenth-century local governments exemplify this dynamic, aggressively modernizing colonial tax regimes while expanding education and health services into ecclesiastical strongholds.

This article is divided into four sections. The first examines the broader historical context of federalism and centralism in Colombia, setting the stage for the analysis of Cundinamarca’s fiscal and social dynamics. The second explores the functioning of federalism in Cundinamarca, focusing on local finances and social expenditure before centralization. The third analyzes the impact of La Regeneración and the shift toward centralism on Cundinamarca’s fiscal and social policies. Finally, the conclusion reflects on the long-term implications of this transition, tying together the economic and political consequences of Colombia’s move from federalism to centralism.

Federalism and centralism in Colombia

Since independence in the 1810s, the tension between centralism and decentralization shaped Latin America’s struggle to forge nation-states with viable governance structures. In Colombia, this process unfolded through alternating constitutional experiments: a confederation (1811-1816), Bolivarian centralism (1821-1831), regionalism under New Granada (1832-1842), conservative centralism (1843-1852), and finally, radical liberal federalism (1853-1886). This cycle culminated in 1884, when a moderate liberal-conservative coalition initiated a recentralization process (Figure 1). The salt and livestock taxes inherited from the colonial era exemplified the system’s regressive impacts. As Van Ausdal (2008) demonstrates, salt was not merely a consumption good but an agricultural necessity – crucial for livestock preservation and cheese production. By monopolizing its distribution and taxing it at 20-30% of market value, the state effectively imposed a disproportionate burden on small farmers and rural laborers, who spent up to 5% of their income on salt alone. Similarly, the alcabala (sales tax) on livestock transactions discouraged protein consumption while generating minimal elite resistance, as large landowners typically self-sufficient in meat production (Van Ausdal 2008, 65-68). These fiscal policies artificially depressed nutritional standards while failing to modernize the tax base.

Figure 1: Constitutions in Latin America 1810-1991

Argentina

1815

1816

1817

1819

1825

1826

1853

1949

1955

Brazil

1824

1891

1934

1937

1946

1967

1969

1988

Chile

1812

1814

1818

1822

1823*

1828

1833

1925

1980

Colombia

1811

1819

1821

1828

1830

1831

1832

1843

1853

1858

1861

1863

1886

1991

Mexico

1812

1814

1824

1835

1836

1843

1847

1857

1917

These transitions were rarely peaceful. Centralism and federalism became ideological battlegrounds for liberal and conservative elites, whose inability to negotiate institutional frameworks civilly precipitated recurrent civil wars. Alongside church-state conflicts, these fiscal-political struggles constituted a primary driver of violence across nineteenth-century Spanish America (Maquard 2009).

Compared to Argentina and Mexico-where richer quantitative and qualitative records exist-Colombia’s nineteenth-century public finances remain understudied. The early republican period (1819-1830) has seen limited analysis, with notable exceptions like Pinto (2011) on regional finances and Junguito (2010) on central-local revenue/expenditure series. For the federal era (1863-1885), Kalmanovitz and López’s (2010) macro-level study of the United States of Colombia has been supplemented by state-level monographs (e.g., Kalmanovitz 2012 on Panama; Pico 2011 on Santander). However, this scholarship disproportionately focuses on tax modernization, leaving expenditure structures-particularly for social services-poorly examined.

Pre-modern states primarily funded military and policing functions, leaving public goods like sanitation and healthcare to private charities. Only in the eighteenth century did governments begin systematically providing merit goods (Lindert 2004). Robert Castell’s concept of the Social State captures this shift: a Durkheimian framework where industrializing societies institutionalized mechanisms to mitigate market inequalities through state-guaranteed protections (Castell 2010). By coordinating antagonistic social interests-employers, workers, the unemployed-the Social State emerged as a mediator of progress (Rose 1999, 135).

The 1850 tax decentralization law marked a watershed, transferring colonial revenue streams (tithes, mining taxes, indigenous tributes, etc.) to provincial control (Melo 2016). This aimed to facilitate abolition of regressive colonial impositions via localized tax reforms. Over the next decade, legislative actions crystallized into the 1863 Constitution, which established the United States of Colombia-a federation of nine sovereign states (Figure 2).

Figure 2. United States of Colombia 1863-1886

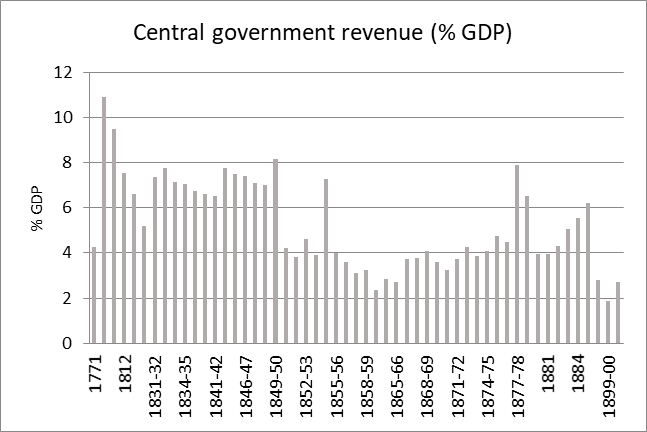

The constitution strictly limited federal powers to defense, education, and interstate infrastructure. States autonomously financed bureaucracy, justice, policing, and growth-oriented expenditures (e.g., education, charities, infrastructure). Federal revenues-initially ~5% of GDP-rose to 8% by 1880 (Figure 3), drawn chiefly from customs (60% of total revenue by 1880), salt monopolies, and railways.

Figure 3. Central Government Revenue (% GDP)

However, this fiscal structure entrenched inequities. Textile import tariffs disproportionately burdened lower classes, while the salt monopoly’s pricing policies provoked widespread farmer resistance. As Van Ausdal (2008) documents, regional rebellions frequently erupted when salt prices exceeded 2 pesos per arroba-a threshold that made basic livestock maintenance economically untenable for smallholders (pp. 72-75). These regressive effects persisted despite federalism’s theoretical promise of more responsive governance.

Federalism in Cundinamarca

During the federal period (1863-1886), state legislatures replaced colonial taxes—including tithes, indigenous tributes, and mining taxes—with modern forms of taxation. These included levies on local trade, liquor production, and direct taxes on incomes and real estate. This transformation formed part of a broader effort to modernize the fiscal system and adapt it to the post-independence economic reality. The federal system granted under the United States of Colombia provided significant fiscal autonomy to its constituent states, making this decentralization not just a political experiment but a practical response to the need for more efficient and locally responsive fiscal administration.

State governments also created specific taxes and contributions to fund public goods such as education, healthcare, and social assistance. For instance, new taxes supported public schools, medical care for the sick, and assistance for children from poor families. These initiatives reflected growing recognition of the state’s role in addressing social needs, particularly in sectors traditionally dominated by the Catholic Church. Progress varied across states, with Cundinamarca, Antioquia, and Cauca emerging as leaders in fiscal modernization and social expenditure. By 1882, these three states showed the highest levels of fiscal autonomy, with Cundinamarca pioneering taxes specifically dedicated to public charity and health initiatives.

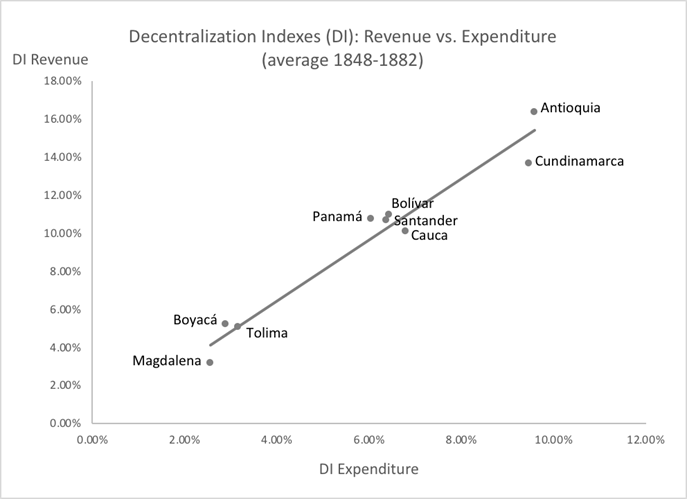

The degree of fiscal decentralization can be measured by comparing subnational government revenues to total national income (Figure 4). On average, state revenues accounted for about 6% of total national tax collection, while subnational public spending reached approximately 10% of total expenditures. This gap between revenue and spending highlights local governments’ reliance on central subsidies and debt financing. Nevertheless, the federal period saw important advances in local administrative capacity and public service expansion. Cundinamarca established a Ministry of Development responsible for public education, infrastructure, and charitable institutions, while Antioquia became the first to implement direct taxes—a model later adopted by the national government.

Figure 4. Descentralization Index (Local taxes as a % of Total Central Government)

Boyacá

Panamá

Cundinamarca

Bolivar

Cauca

Tolima

Magdalena

Santander

Antioquia

1848

0.4%

0.4%

0.9%

1.3%

1.1%

0.4%

0.3%

1.4%

2.1%

1851

1.9%

5.2%

4.5%

6.8%

5.1%

2.6%

1.5%

10.0%

2.6%

1856

2.2%

7.6%

4.3%

5.9%

6.2%

2.8%

3.1%

5.1%

7.6%

1870

4.0%

11.3%

13.1%

8.9%

8.1%

4.5%

2.7%

7.2%

13.1%

1873

3.1%

8.1%

11.3%

5.2%

4.1%

3.9%

2.0%

6.0%

10.2%

1874

3.2%

8.4%

11.6%

n.a

n.a

n.a

n.a

n.a

10.4%

1876

5.1%

5.8%

14.9%

8.1%

9.0%

4.6%

3.9%

n.a

14.6%

1882

3.4%

4.9%

15.2%

6.2%

14.2%

3.5%

4.3%

8.6%

16.2%

Source: Kalmanovitz and López 2010, State of Cundinamarca. Laws and Department Council Ordinances 1862-1911.

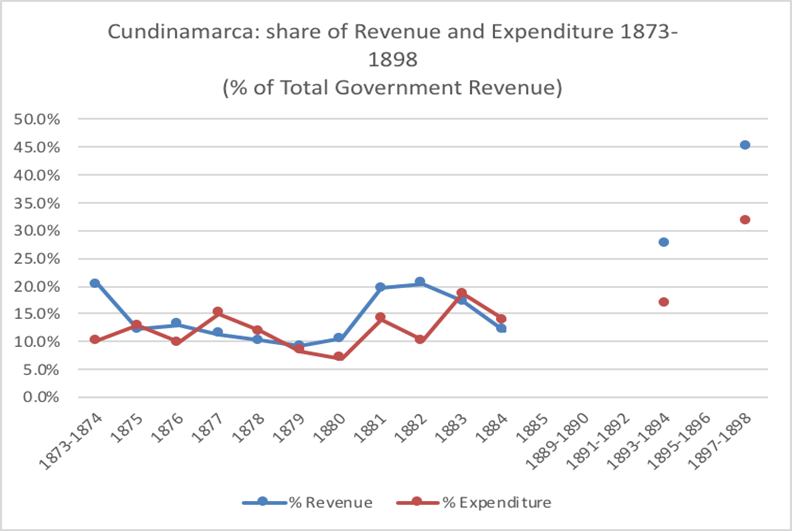

The decentralization process reflected each state’s unique economic and institutional context. Cundinamarca benefited from its proximity to Bogotá and relatively developed infrastructure, while Antioquia relied on gold mining revenues and Cauca on agricultural production. These regional differences underscore how local conditions shaped fiscal policies. However, decentralization also created challenges, including fiscal imbalances, inefficiencies, and political conflicts between state and central governments. By 1882, Antioquia, Cundinamarca and Cauca showed the highest levels of fiscal autonomy (Figure 5). Across all states, average revenues reached 6% of national collections, while public spending accounted for 10%.

Figure 5

Source: Kalmanovitz and López 2010, State of Cundinamarca Laws and Department Council Ordinances 1862-1911.

Cundinamarca made significant progress in building its administrative framework. By 1881, the executive branch comprised three key offices: Government, Development, and Treasury. The Ministry of Development oversaw public education, road construction, postal services, and charitable institutions. The legislative branch included representatives from all regions of the state, with their expenses covered by the executive.

The fiscal modernization process in Cundinamarca during the federal period exemplified the institutional dynamics theorized by Acemoglu et al. (2001) discussed in Section 1. As states replaced colonial taxes with modern systems, they developed precisely the kind of inclusive fiscal institutions that promote long-term development. Cundinamarca’s innovative taxes for social spending—particularly its 1870s charity levies—demonstrated how subnational governments could respond more effectively to local needs than centralized bureaucracies (Oates 1999), though within the constraints highlighted by Stein (1998).

The 1879 loan agreement, negotiated during this transitional period, reveals both the possibilities and limitations of state-level fiscal autonomy. Contracted with private Bogotá bankers at 6% annual interest, the 50,000-peso loan carried a three-year maturity and was specifically earmarked for judicial department operations, particularly prison maintenance. This conditional financing mirrored practices in Argentina’s provincial debt crises of the 1880s (Newland 1998), but with stricter repayment guarantees: 30% of Cundinamarca’s liquor tax revenues served as collateral. Such arrangements reflected the « productive state » role described by Dincecco and Katz (2012), where governments balanced extractive capacity with public goods provision.

These fiscal innovations occurred amidst Colombia’s broader centralization debate. While the 1886 Constitution would later recentralize power, Cundinamarca’s 1874-1885 expenditure records show how federalism temporarily enabled the « Social State » functions Castell (2010) identified—with education and charity spending growing from 18% to 22% of budgets despite wartime pressures. The state’s 1879 decision to fund judicial reforms through earmarked debt rather than church partnerships (unlike early 19th century models) marked a decisive shift toward secular institutionalism.

In terms of fiscal performance, Cundinamarca’s average tax revenue ranked second among states during 1856-1886, slightly behind Antioquia. While its 1848 revenue levels resembled other states, Cundinamarca achieved nearly 10% average annual growth—the highest rate among all sovereign states (Figure 6). By 1873, the majority of its tax revenue came from tolls (36%), direct contributions (18%), consumption taxes (17%), and the degüello (slaughter tax, 14%). Both Cundinamarca and Santander pioneered direct taxation, which the central government would later implement through Law 56 of 1918 (Díaz 1997). However, toll collections simultaneously hindered internal market development.

Figure 6.

Source: State of Cundinamarca. Laws and Department Council Ordinances 1862-1911.

Public expenditure focused primarily on operational costs, defense, and road infrastructure, though spending on public charity and education gradually increased. From 1874 to 1885, expenditure trends rose steadily, particularly during the 1876-1877 war. This conflict emerged from multiple factors: the global economic crisis beginning in 1873 depressed tobacco and gold exports, radical liberal governments faced growing opposition after fourteen years in power, and conservatives strongly resisted liberal education reforms promoting secular, free, and compulsory schooling. Cundinamarca became a key battleground, with significant guerrilla activity in Mochuelos and Guascas (Ortiz 2004).

Despite revenue growth, tax collections failed to cover all state expenses. Fiscal deficits necessitated additional borrowing from local lenders, national subsidies, or central government loans. For example, funds from an 1879 loan supported judicial department expenses for local prisons. In 1874, the government allocated substantial resources to compensate victims of that year’s war through treasury and charitable department expenditures—all financed through debt. As the federal period drew to a close in 1884, new loans primarily funded transportation infrastructure and executive branch operations. Once again, political instability explains both volatile revenue streams and persistent fiscal deficits.

Centralization and “La Regeneración”

By 1880, the political pendulum began to swing away from Liberal anticlerical excess and toward a more Conservative-unitarian structure. This shift coincided with the rise of Rafael Núñez, who was elected president that year. A native of Cartagena in northern Colombia, his election marked an important regional shift away from the traditional leaders from the central highlands who had dominated federal politics. Núñez was reelected in 1884, and when Radical Liberals revolted against his government the following year, he used this as justification to dissolve the 1863 Constitution. His « Regeneration » movement became the political platform for a prolonged period of Conservative rule that sought to reestablish a unitary state governed from Bogotá. The new 1886 Constitution strengthened the central executive and restored the power and prestige of the Roman Catholic Church, attempting to rectify the problems created by the decentralized, federalist, and anticlerical 1863 Constitution.

The central government’s reassertion of fiscal control proceeded gradually but systematically. In the 1890s, revenue from cattle slaughter taxes returned to central control, and in 1892, new domestic taxes were imposed on cigarettes and other goods. By 1897, while states regained control over slaughter taxes, they did so without taking on additional responsibilities, as the national government had already assumed control over policing (through the creation of the national police in 1891) and secondary education. Throughout this period, customs duties remained the primary source of revenue, followed by income from salt mine leases.

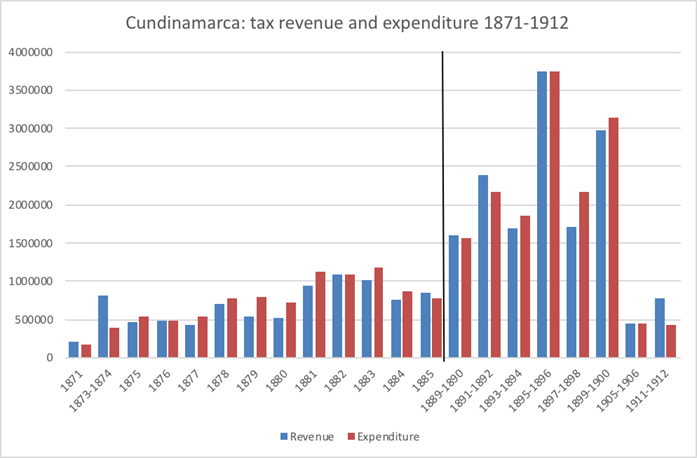

Figure 7

Source: State of Cundinamarca. Laws and Department Council Ordinances 1862-1911.

Despite these centralizing reforms, the transition to a fully centralized fiscal state was not immediate—particularly in Cundinamarca. Cundinamarca had developed robust fiscal institutions during the federal period, with tax revenues growing at an average annual rate of 10% between 1856 and 1886. This institutional strength allowed the department to maintain significant fiscal autonomy even after 1886. Both revenues and expenditures continued to grow as a share of central government totals, and the local legislature retained authority to collect direct taxes and slaughter taxes, as well as to allocate subsidies for public schools, hospitals, and lazarettos (Figure 7).

This continuity reflects the patterns observed in Section 2, where Cundinamarca had emerged as a leader in fiscal innovation and social spending. During the federal period, the department had pioneered taxes specifically earmarked for public charity, and this institutional legacy proved durable. While civil wars persisted during the transition to centralization, Cundinamarca’s administrative framework—including its Ministry of Development and Treasury—remained intact, allowing it to continue managing key expenditures locally.

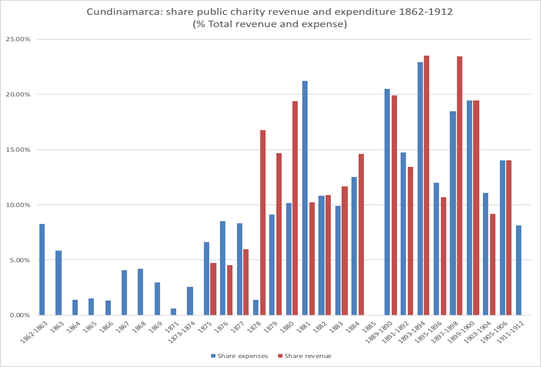

The central government faced significant challenges in assuming full control over the fiscal responsibilities that had been developed at the subnational level. This difficulty resulted in a de facto decentralization that persisted until at least 1910, when major constitutional reforms were introduced. Even then, as demonstrated in Figure 8, Cundinamarca’s public charity expenditures remained a consistent share of its budget, underscoring the department’s ongoing role in social welfare provision.

Figure 8

Sources: State of Cundinamarca. Laws and Department Council Ordinances 1862-1911.

The persistence of local fiscal autonomy in Cundinamarca can be attributed to several factors, all of which build on the foundations established during the federal period (as detailed in Section 2):

Political and Economic Factors: The department’s relatively prosperous economic base and the political importance of social spending created strong incentives to maintain local control.

Institutional Legacy: The tax systems and administrative structures developed before 1886 proved resilient, enabling continued local revenue generation.

Central Government Limitations: Bogotá lacked the capacity to immediately absorb all subnational functions, particularly in areas like health and education where Cundinamarca had long been active.

This continuity is particularly evident in public charity expenditures, which remained a priority for Cundinamarca throughout the centralization process. Historical records show that hospitals, hospices, and other welfare institutions continued to receive stable funding, reflecting the department’s enduring commitment to social welfare—a commitment that had first emerged during its federal-era innovations.

The Colombian experience illustrates the broader tensions between centralization and decentralization in Latin American state-building. While the 1886 Constitution sought to create a more unified fiscal system, the reality was more complex, with regions like Cundinamarca retaining substantial autonomy. This aligns with the patterns observed in Section 2, where federalism had allowed subnational governments to develop fiscal and administrative capacities that proved difficult to dismantle. Even after the 1910 reforms, Cundinamarca’s social spending remained significant, demonstrating the lasting impact of its federal-era institutions.

Conclusion

The case of Cundinamarca during the late 19th and early 20th centuries provides a compelling illustration of three fundamental dynamics in institutional development. First, it demonstrates the remarkable resilience of local institutions – even under formal centralization, Cundinamarca’s fiscal systems, developed during the federal period, maintained their capacity for social spending and adaptation. This persistence challenges conventional assumptions about the inevitability of top-down control in state-building processes.

Second, the department’s experience reveals a crucial paradox regarding inclusive institutions. While Cundinamarca’s tax-funded charity programs exemplify the kind of inclusive institutions that Acemoglu, Johnson, and Robinson identify as drivers of development, their survival ultimately depended on an unstable equilibrium created by central state weakness. This tension between local responsiveness and national cohesion remains highly relevant for understanding governance challenges in developing states today.

Third, the Colombian case highlights the limits of institutional transplants. The 1886 centralization attempted to impose a unitary model on a society profoundly shaped by federalism. Cundinamarca’s experience shows how deeply institutional legacies can constrain such transformation efforts, offering important lessons for contemporary policymakers.

The federal period following the 1863 Constitution enabled Cundinamarca to pioneer innovative fiscal policies, particularly taxes earmarked for public charity and health initiatives. When the 1886 Constitution sought to reverse this decentralization, recentralizing power in Bogotá, the transition proved neither immediate nor absolute. Cundinamarca retained significant fiscal independence well into the early 20th century, continuing to fund hospitals, schools, and welfare programs through adapted versions of its federal-era systems.

This historical trajectory reflects broader patterns in Latin American state-building. The oscillation between centralism and federalism, frequently interrupted by civil conflicts, underscores how contested institutional development has been in the region. While the Regeneration governments of the 1880s-1890s attempted to impose fiscal uniformity, their efforts encountered persistent resistance in regions like Cundinamarca where local governance structures had taken root.

From a theoretical perspective, Cundinamarca’s experience both confirms and complicates existing frameworks. It supports the argument that inclusive institutions promote development, yet reveals how their sustainability may depend on broader political conditions. The department’s ability to maintain social spending despite civil conflicts suggests that local institutionalization can sometimes withstand macropolitical instability.

Three key insights emerge from Cundinamarca’s case that reshape our understanding of state-building. First, it demonstrates how federalism’s institutional legacy can shape long-term development trajectories. Second, it reveals how social spending becomes contested terrain between competing governance visions. Third, it shows how civil conflict erodes – yet does not eliminate – local fiscal capacity. These findings suggest contemporary decentralization debates must consider Colombia’s historical experience of institutional duality, where formal and de facto power structures rarely achieved perfect alignment. Future comparative research could productively examine these patterns in other contexts where centralization confronted entrenched local systems, such as post-Revolutionary Mexico or Weimar Germany.

References

Primary Sources

Informe del gobernador de la Provincia de Bogotá 1856. Presupuesto provincial de gastos para el servicio del año económico de 1856 a 1857.

Informe del Secretario de Gobierno de Cundinamarca. 1863.

Tercer Informe Anual del director de la Instrucción Pública del Estado Soberano de Cundinamarca. Año de 1873.

Informe del Secretario de General al Gobernador de Cundinamarca 1873

Decreto 130 de 1878 sobre liquidación de gastos del presupuesto de 1879.

Memoria del secretario de hacienda del Estado soberano de Cundinamarca. 1879.

Leyes de presupuesto de rentas y gastos de los años: 1857, 1859, 1863, 1864, 1866, 1867, 1868,1869, 1870, 1874, 1875, 1876, 1877, 1878, 1880, 1881, 1882, 1883, 1884, 1887-1912.

Secondary Sources

Acemoglu, D., Johnson, S., & Robinson, J. A. (2001). The colonial origins of comparative development: An empirical investigation. American Economic Review, 91(5), 1369–1401. https://doi.org/10.1257/aer.91.5.1369

Acemoglu, D., Johnson, S., & Robinson, J. A. (2005). Institutions as the fundamental cause of long-run growth. In P. Aghion & S. N. Durlauf (Eds.), Handbook of economic growth (Vol. 1A, pp. 385–472). Elsevier. https://doi.org/10.1016/S1574-0684(05)01006-3

Bardhan, P.; Mookherjee, D. (2005). Decentralization, Corruption and Government Accountability: an overview, Handbook of Economic Corruption.

Brueckner, J. (2001). “Fiscal Decentralization in Developing Countries: the Effects of Local Corruption and Tax Evasion”, Annals of Economics and Finance , vol. 1, núm. 18, Universidad de Illinois.

Castel, Robert. El Ascenso de las Incertidumbres. Trabajo, Protecciones, Estatuto del Individuo. México: Fondo de Cultura Económica. 2010.

Castillo, Adriana y Edwin López. 2012. « Federalismo y reformas institucionales en Cundinamarca 1848-1890.” En: Documentos de Trabajo en Economía. Bogotá: Universidad Jorge Tadeo Lozano.

Clavijo O., H. “Monopolio fiscal y guerras civiles en el Tolima, 1865-1899”, Boletín Cultural y Bibliográfico 30, 32, 1993.

Díaz, Sylvia Beatriz. 1997. Finanzas Públicas del gobierno central en Colombia 1905 – 1925. Historia Crítica. No 14. Universidad de los Andes.

Dincecco, Mark y Gabriel Katz 2012. “State Capacity and Long-Run Performance”. Berkeley Economic History Laboratory. Working Paper Series. Wp2013-01.

Domínguez Osa, Camilo. Inserción de Colombia en la Economía Mundo y su Influencia sobre la Construcción del Estado Nación. En: Scripta Nova Revista Electrónica de Geografía y Ciencias Sociales Universidad de Barcelona. 418 (59), 1 de noviembre de 2012.

Dye, Alan, 2006 “The Institutional Framework”, in Bulmer-Thomas et al. (eds.), The Cambridge Economic History of Latin America, vol. 2, p. 189.

Fisman, R.; Gatti, R. 2002. “Decentralization and Corruption: Evidence Across Countries”, Journal of Public Economics , vol. 83, núm. 3, pp. 325-345.

Iimi, A. 2005. “Decentralization and Economic Growth Revisited: An Empirical Note”, Journal of Urban Economics , vol. 57, núm. 3, pp. 449-461.

Hermandez, Mario 2004. « La Fragmentación de la Salud en Colombia y Argentina. Una Comparación Sociopolitica, 1880-1950. » Bogotá: Universidad de los Andes.

Junguito, Roberto (2010). Las finanzas públicas en el siglo XIX. En Meisel A y Ramirez, M. (Eds.), Economía colombiana del siglo XIX (pp. 41-136). Bogotá: Banco de la República y Fondo de Cultura Económica.

Kalmanovitz, S. y López, E. (2010). Las finanzas públicas de la Confederación Granadina y los Estados Unidos de Colombia, 1850-1886. Revista de Economía Institucional, 12 (23), 199-228.

Kalmanovitz, S. (2012). El federalismo y la fiscalidad del Estado Soberano de Panamá, 1850-1886. Revista de Economía Institucional, 14 (27), 99-145.

Kergelen, Ricardo 2014. “Political Discourses, Territorial Configuration and Taxation: Conflicts in Antioquia and Cauca, Colombia (1850-1899).” Doctoral Dissertation. UC San Diego.

Lindert, Peter. 2004. Growing Public: Volume 1, The Story: Social Spending and Economic Growth Since the Eighteenth Century. Cambridge University Press. 2004.

Marquardt, Bernard 2009. El federalismo y el regionalismo en el constitucionalismo hispanoamericano (1810 – 2009): ¿patria boba o un camino para profundizar la democracia? Revista Pensamiento Jurídico, 24.

Melo, Jorge Orlando. “Las vicisitudes del modelo liberal (1850-1899).” In Ocampo, José Antonio. Historia Económica de Colombia. Fondo de Cultura Económica. Bogotá. 2016.

Monroy, Claudia Liliana 2010. “De Federalismo a Regeneración. El paso de Estados Soberanos a Departamentos Político-Administrativos. Boyacá, 1886-1903” En: Historelo Revista de Historia Regional y Local, Volumen 4, Número 7, p. 218-239.

Oates, W. (1999). “An essay on fiscal federalism”, Journal of Economic Literature , núm. 37, pp. 1120- 1149.

Ortiz Mesa, Luis Javier. 2004. Fusiles y Plegarias. Guerra de guerrillas en Cundinamarca, Boyacá y Santander, 1876 – 1877. Universidad Nacional de Colombia.

Pinto, J. (2011). Finanzas de la República de Colombia, 1819-1830. (Tesis de maestría inédita). Universidad Nacional de Colombia, Bogotá.

Rose, Nikolas. Powers of Freedom: Reframing Political Thought. Cambridge University Press. 1999.

Safford, Frank and Palacios Marco 2002. “Colombia Fragmented Land Divided Society” Oxford University Press.

Stein, E. (1998). “Fiscal Decentralization and Government Size in Latin America”, Working Paper, Inter-American Development Bank , núm. 368.

Tiebout, C. (1956). “A pure theory of local expenditures”, Journal of Political Economy , vol. 64, núm. 5, pp. 416-424.

Tulchin, J.; Selee, A. (2004). “Decentralization and Democratic Governance in Latin America”, Wilson Center Reports on the Americas , núm. 12, Woodrow Wilson International Center for Scholars.

Van Ausdal, S. “Un mosaico cambiante: notas sobre una geografía histórica de la ganadería en Colombia, 1850-1950”, A. Flórez M., ed., El poder de la carne, Bogotá, Pontificia Universidad Javeriana, 2008.

Weingast, B. (1995). “The Economic Role of Political Institutions: Market-preserving federalism and economic development”, The Journal of Law , Economics and Organization, núm. 11.